The UK property market has been facing challenges in recent months as rising interest rates have pushed lenders to increase the cost of borrowing accordingly. Although it may seem daunting now — with the right advice your clients may be able to navigate any potential issues with calmness and confidence.

Staying calm in the face of pressure is a lesson that one of the golfing greats had to learn before he could triumph.

We’re not talking about Tiger Woods, Jack Nicklaus, or Arnold Palmer — we’re talking about the legend that is Happy Gilmore.

Now we do understand that Happy is a fictional character, but his journey to golfing greatness has some useful similarities to the challenges facing many UK homeowners.

Happy’s grandmother faced losing her home, so he sought an “out of the box” solution and worked on having a positive mentality to eventually reach his goal of saving her property.

Read on to discover some of the challenges your clients might face in the current UK mortgage market, and how Happy Gilmore and a creative fixed-fee solution could be the key to overcoming them.

The UK property market is volatile at the moment

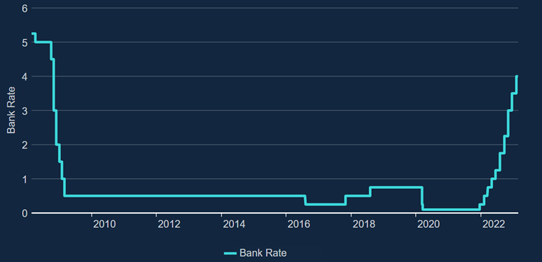

A myriad of macro and microeconomic factors led to inflation in the UK reaching a high of 11.1% in the year to October 2022, according to Office for National Statistics (ONS) figures.

In a move to combat the rising cost of living, and encourage savings, the Bank of England (BoE) have increased the base rate 10 times since it was cut to an all-time low at the start of the pandemic in March 2020, as shown by the graph below:

Source: BoE

The rising base rate has prompted lenders to increase their respective rates. Following the UK government’s autumn statement, mortgage rates spiked to over 6% before a competitive market pushed rates back down slightly.

According to the Guardian, many lenders fear a sharp rise in mortgage defaults in 2023, as many households on variable-rate mortgages struggle with increased monthly costs. Anyone with a fixed-rate deal maturing in the near future could find themselves in the same situation soon.

Happy Gilmore was presented with a similar problem when the IRS came knocking on his grandmother’s door with an outstanding $270,000 tax bill and a foreclosure notice — a prescient reminder for your clients to pay their taxes in a timely manner — and faced with losing their home, he came up with an alternative solution to their problems.

Happy decided to try and pay off their debts by winning golf tournaments. But could your clients’ find a creative “hole in one” solution in the benefits of fixed fees?

Fixed fees offer your clients honest and transparent advice on how to solve their problems

Now, to be clear, when we refer to fixed fees, we aren’t talking about fixed rates on mortgages. Your clients should consider reviewing their agreements first and sourcing the best possible rates whether that is continuing on a variable-rate deal or finding new fixed-rate terms.

However, with a more costly mortgage market, a new agreement is likely to only put a cap on the potential rising costs your clients might face. Working towards securing their long-term futures and avoiding the risk of default might require further steps.

At Grey Parrot, we like to work a little bit differently. If your clients are Happy Gilmore in this analogy, we’re his wise old golf coach Chubbs, played by Rocky legend Carl Weathers. We’re here to guide them towards the best possible outcomes.

Good financial planning relies on us building a trusting and long-term relationship with your clients. One way we achieve this is through honest and transparent charges.

Traditionally advisers charge percentage-based fees. Over the long term, these can see your clients paying out increasing amounts, while the work done by their advisers remains largely the same — percentages are like variable-rates.

A fixed-fee approach means your clients pay the same amount for the respective work done.

2 creative ways fixed fees can help your clients with their mortgage costs

1. Fixed fees remove financial incentives from your clients’ advisers decision-making process

Percentage-based fees incentivise your clients’ advisers to push for greater gains, despite increased risks, or to recommend certain financial products in order to grow their respective fees.

Fixed fees put the focus firmly on your clients’ needs and goals first, and any solutions second.

This emphasises reducing potential risks, streamlining your clients’ outgoings, and growing their wealth in a sustainable and evidence-supported manner.

This added focus and oversight can help your clients’ find ways to mitigate any rising mortgage costs by making alterations elsewhere in their financial plans.

2. Fixed fees reduce your clients’ costs and offer long-term stability

If your clients invested £250,000 with a percentage-based planner and over 10 years the value of their investments increase to £500,000, the amount they pay will have doubled, even though their adviser is essentially doing the same amount of work.

At Grey Parrot, we charge a fixed fee, adjusted for inflation. So, in 10 years’ time, even if the value of your clients’ investments has multiplied, their fees won’t have changed in real terms.

Additionally, the extra funds freed up through a fixed-fee model could potentially be assigned to other vital outgoings, such as covering mortgage payments.

We like to refer to these extra funds as “the wedge”. In fact, we call it “Reg the Wedge”.

In working with a fixed-fee model, we can help your clients rescue their wedge. It could end up being the most important act in achieving their long-term goals.

In the end, Happy’s creative approach to his grandmother’s housing issue succeeded and he was able to pay off her debts, while also becoming the PGA champion.

Fixed fees won’t solve all your clients’ problems, but they just might put them within putting distance of their long-term goals.

Get in touch

If you or your clients are worried about rising mortgage costs, seeking professional advice could be key to mitigating issues and staying on course towards long-term goals.

A good first step could be to reach out by email at info@grey-parrot.co.uk or call us at 02039 871782.

Please note

This article is no substitute for financial advice and should not be treated as such. To determine the best course of action for your individual circumstances, please contact us.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

Buy-to-let (pure) and commercial mortgages are not regulated by the FCA.

Think carefully before securing other debts against your home.

Production

Production