One of the most significant gifts your clients can give their loved ones comes in the form of inheritance. It can be sizeable boost to their finances and potentially life-changing.

If your clients’ wealth can provide happiness and help to their loved ones, why wait until they’re gone?

Gifting while they’re still alive, gives your clients the opportunity to see the benefits to their loved ones’ lives first-hand.

It is a valuable idea, especially as the amount of money Brits are paying in Inheritance Tax (IHT) is higher than ever. According to the Office for Budget Responsibility (OBR)’s economic and fiscal outlook for the next five years, UK families could end up paying £37 billion in IHT – a 36% increase on the sum paid between 2017 and 2021.

This is largely because even though average estates have grown in size, the threshold for paying IHT has remained the same.

Read on to discover five promising ways your clients can use gifting to reduce their potential tax liability and help loved ones in the process.

1. Your clients could utilise the annual gifting exemption of £3,000

In the 2022/23 tax year, your clients have a gifting exemption of £3,000. This means they can give away this amount and it will immediately fall outside of their estate for IHT purposes.

The annual exemption can be passed onto the subsequent year. So, if your clients didn’t utilise it in the 2021/22 tax year, they could gift £6,000 this year.

It is a benefit that doubles down for your clients if they are part of a couple, as the £3,000 individual exemption becomes £6,000 that partners can gift each year.

As RuPaul, once said: “The whole point is to live life and be. To use all the colours in the crayon box”. By utilising their annual exemption, your clients could help their loved ones live their ideal lives and be there to witness all their milestones and experiences.

2. Your clients could benefit from the “seven-year” rule

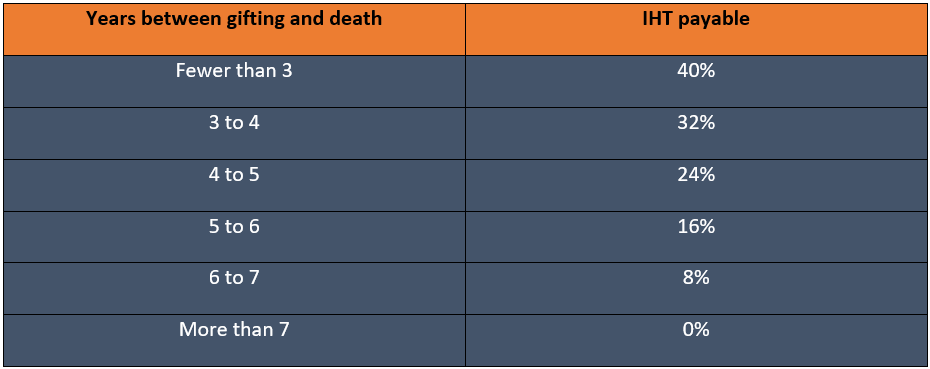

Provided your clients live for at least seven years from the date of making a gift they could in theory gift as much money as they’d like to loved ones without it typically being subject to IHT.

In this scenario, the gift becomes what is known as a “potentially exempt transfer” (PET).

However, if your clients were to die within seven years, the gift might become a “chargeable transfer” and their estate may be required to pay some IHT.

The amount of IHT payable gradually reduces between three and seven years, so the longer your clients live following gifting, the less tax their estate could have to pay.

The reductions across this time period are known as “taper relief” and are detailed in the table below:

Usually, your clients’ estate will pay 40% IHT on any wealth above the nil-rate band of £325,000 (or £500,000 if they plan to leave their home to a child or grandchild). The taper relief only applies to gifts in excess of this threshold. It should also be noted that taper relief doesn’t reduce the value of the transfer — it only reduces the tax liability on that transfer.

So, it might be a good idea for your clients to keep accurate and detailed records of their gifting including:

- The date of the gift

- The beneficiary

- The amount that your client gifted.

This will be beneficial for their executor during probate, as they will need to calculate the amount of IHT payable.

3. Your clients could make small gifts of £250 or less

In the words of Tesco: “every little helps”. The supermarket slogan makes an important point, that even the smallest gifts can be hugely beneficial to those involved.

Your clients can make small gifts up to and including £250, to any individual, that are not subject to IHT. They also do not form part of their £3,000 annual exemption.

4. Your clients could gift from their income

One special feature of IHT rules is the exemption for “normal expenditure out of income”. This means that regular gifts out of your clients’ income, such as meeting care costs for a relative, or saving for children or grandchildren into an ISA or JISA, might be free from IHT.

Your clients must meet the following requirements to qualify for this exemption:

- The gift must come from their income

- The gift must be part of their normal outgoings — they may need to demonstrate it is a regular amount going out on a regular date

- The gifting should not inhibit your clients’ regular standard of living.

This exemption can be tricky to obtain and so it is vital that your clients keep accurate financial records, especially regarding any ongoing gifts, in order to qualify.

Ensuring any regular gifts are recorded in a written agreement can help your clients with the process and help their executors make calculations in the future.

5. Your clients could gift as part of a wedding or civil partnership

A wedding or civil partnership ceremony on the horizon provides your clients with an opportunity to make a gift to the couple that will fall outside any potential IHT on their estate.

It is important that your clients make the gift before the wedding and that the ceremony eventually takes place in order to qualify for the IHT exemption. The amounts your clients can gift are as follows:

- Up to £1,000 to an extended family member or friend

- Up to £2,500 to a grandchild or great-grandchild

- Up to £5,000 to a child.

Get in touch

Saving is a key part of the Grey Parrot ethos. Whether it’s reducing taxes, making less costly investments, or lowering clients’ financial planning charges with a fixed-fee approach.

If your clients could benefit from making savings in the short or long term, they should contact us by email at info@grey-parrot.co.uk or call us at 02039 871782.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.

Remember that taper relief only applies to gifts in excess of the nil-rate band. It follows that, if no tax is payable on the transfer because it does not exceed the nil-rate band (after cumulation), there can be no relief.

Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.

Production

Production