Memories shape lives and influence key decisions. They hold within them the sum total of someone’s experiences and knowledge. Yet despite our memories being crucial to decision-making, they can often be unreliable and flawed.

Your clients will undoubtedly have heard the old idioms “an elephant never forgets” and “the memory of a goldfish” at some point in their lives. Yet, they might not have realised how important the difference is when it comes to the world of investing.

Many investors act like goldfish — only recalling the short term — and remain firmly focused on the present. Others adopt the mindset of an elephant and remember long-term facts and details.

Read on to discover two proven reasons why learning to think a little bit like both might be beneficial for your clients’ investments.

1. “Memory of a goldfish” — your clients should have a short-term memory when it comes to failure and success

Investing offers the potential for great returns, as your clients put their hard-earned money to work by funding investments. Working alongside a financial planner can mitigate risk. This is an important move as financial gains can’t be guaranteed and the potential for losses can’t be completely eliminated.

It is important for your clients to remember that before they make any investing decisions.

Markets typically ebb and flow and have the potential to be volatile. So, it is possible that in the short term your clients might celebrate significant successes or regret painful losses.

These highs of gains and lows of losses can prompt psychological biases in investors and in doing so negatively affect their long-term outlook. That’s why it is vital that your clients adopt a goldfish’s mindset when it comes to the short term.

The overconfidence effect can push your clients to take too much risk

Confidence is a great trait to possess, while overconfidence can lead to mistakes. “The overconfidence effect” is a psychological bias that skews a person’s perception by imbuing them with a positive belief in their judgement that is greater than the actual objective accuracy of those judgements.

A study in the American Journal of Psychology showed that overconfidence can produce a significant error rate in actual results. The difference between the participants’ belief they were correct about the spelling of words in the study and their actual results showed they were wrong 20% of the time, even though they claimed near or absolute certainty they were correct. The margin of error remained the same when tested against true or false questions.

If your clients have a string of short-term investing decisions that produce significant returns, they may fall victim to this bias and believe they can continue to predict the market.

They may even be influenced by additional biases such as:

- “Confirmation bias” which would see them seek out supporting data to back up their intended decisions, ignoring anything to the contrary

- “Herd behaviour” in which they confidently jump on an investing trend that their peers recommend, such as investing in cryptocurrency or NFTs

- “Recency bias”, in which they favour recent events over historic ones.

This mentality is commonplace at casino tables, as each subsequent win encourages gamblers to push for more. It is incredibly risky for your clients to adopt this mindset when investing and could lead to larger potential losses.

Losses are likely to push your clients to tighten their belts and cut their outgoings, which may mean reducing pension contributions or cancelling their insurance.

Remember: your clients should know there’s no “sure thing” when investing.

Your clients could benefit from starting each day anew and not letting short-term memories hold too much sway over them. Your clients should be “a little bit goldfish”.

2. “An elephant never forgets” — history provides guidance and shows that a long-term outlook will likely benefit your clients

While in the short term your clients’ memories should be quick to put ups and downs behind them, over the long term it could benefit them to think like an elephant and never forget some key lessons from the distant past.

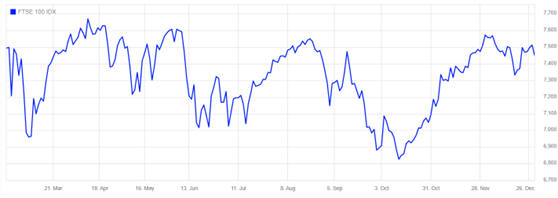

In the short term, markets tend to be volatile even at the best of times. A look at the FTSE 100 over the course of 2022 shows it frequently going up and down.

Source: London Stock Exchange

However, if we pull back and look at a 20-year period through to the end of 2022, the graph below tells a very different story:

Source: London Stock Exchange

Investors that decided to sell off their portfolios in 2009 or in the spring of 2020 would have missed out on the gains likely produced on their investments when the markets recovered and continued in a long-term upwards trajectory.

If they opt instead for a passive, “buy-and-hold” approach, they are likely to ride out short-term volatility and be positioned to make gains in the long term.

Research from Nutmeg details how if your clients picked one random day to invest and held the investment for 24 hours, their chances of positive returns would be 52.4%. If they held this same investment for 10 years, their chances would nearly double to 94.2%.

Get in touch

If you’re worried that your clients are overly concerning themselves with short-term problems and losing sight of the bigger picture, it might be worth recommending they seek out a financial adviser.

Financial advice can improve their emotional wellbeing and set them on the right path for their long-term goals. The first step might be contacting us at info@grey-parrot.co.uk or calling 02039 871782.

Please note

This article is no substitute for financial advice and should not be treated as such. To determine the best course of action for your individual circumstances, please contact us.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Production

Production