Your clients will probably recognise the iconic “death and taxes” quote, but they might not have heard this pearl of wisdom from Albert Einstein: “The hardest thing in the world to understand is the Income Tax”.

According to MoneyAge, 2 million Brits are facing the possibility of paying an effective 60% marginal Income Tax rate by 2028 due to the recent freeze on UK tax thresholds.

If your clients have spent their careers working hard and building up sizeable incomes, they’ll probably not be keen on the prospect of potentially seeing over half of their earnings lost to taxation.

However, it is important that they stay calm. There are many ways to build tax relief into their financial plans and ensure they remain on course to meet their long-term goals.

One particularly effective option is pension contributions.

Read on to discover how the government’s 60% tax trap has arisen and why pension contributions could play a crucial role in protecting your clients’ income.

An effectively 60% tax rate has been created for some high earners by the tapering of the Personal Allowance

If your clients earn between £100,000 and £125,140 a year, they could be exposed to an effective tax rate of 60% due to a quirk created by recent updates to Income Tax rules.

This 60% “tax trap” is a consequence of the tapering of the Personal Allowance for high earners.

The Personal Allowance stands at £12,570 for the 2022/23 tax year. If your clients earn £100,000 or more, the rate of Income Tax they pay will be affected by the tapering of the Personal Allowance.

The allowance is currently tapered at a rate of £1 for every £2 your clients earn above £100,000.

This creates a scenario at the 40% higher rate of Income Tax — on earnings between £100,000 and £125,140 — in which the combination of taxes and reduction in allowances leads to an effective tax rate of 60%.

For example, for every £1,000 of income between £100,000 and £125,140, your clients only take home £400 — £400 is lost to Income Tax, and another £200 is removed by the tapering of their Personal Allowance.

Once your clients surpass £125,140 of earnings, they no longer benefit from any Personal Allowance, so they avoid the unfortunate sinkhole created by an awkward overlap of two different tax policies.

If your clients would prefer not to pay a tax rate of 60%, which we imagine is the case, there are a few ways they can make up the tax relief elsewhere. One of the most compelling is pension contributions.

Your clients could consider using the tax relief benefits of pension contributions to beat the 60% tax trap

Paying into a pension scheme is one of the most tax-efficient ways your clients can save towards their eventual retirement. The benefits can be substantial and may help offset the adverse effects of a potentially sizeable Income Tax bill.

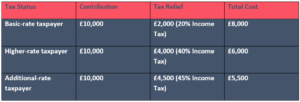

For high earners, the value of tax relief becomes increasingly attractive as shown by the table below:

It should be noted that while any basic-rate relief is paid automatically, if your clients qualify as a higher- or additional-rate taxpayer, they may need to claim their further 20% or 25% through a self-assessment tax return.

Your clients can typically save up to £40,000 each tax year into their pensions (or 100% of their earnings if lower) and receive tax relief from the UK government.

Opting to make pension contributions can have a wide range of additional benefits for your clients:

- Potential for “free money” in the form of employer contributions to their workplace pension, which stands at least 3% and could be higher if their employers choose to increase their percentage in line with your clients’ contributions

- Long-term benefits of compound returns on the value of their pension pots

- Added protection against any possible retirement income shortfall.

Pension contributions can have significant tax benefits and are a vital component of a solid financial plan. They can go a long way towards keeping your clients on course to meet their long-term retirement and lifestyle goals.

Read more: 3 important advantages of financial planning

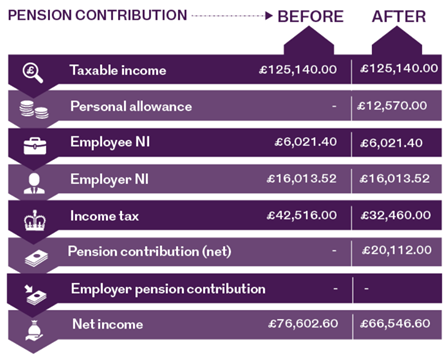

According to Royal London, increasing pension contributions could be a beneficial solution to your clients’ problems caused by the tapering of the Personal Allowance between £100,000 and £125,140.

At £125,140, a pension contribution of £25,140 (including the basic-rate tax relief) results in a reduction to net income of just £10,056. This provides an effective tax relief rate of 60%, as shown in the table below.

Source: Royal London

It is possible that the additional contributions your clients could opt to make may be crucial in negating any possible tax complications arising from the 60% tax trap and could provide not only incredibly valuable tax relief, but also emotional relief.

At Grey Parrot, we understand that people worry about lots of things, but at their core, there are three constant worries — family, health, and money.

Through making smart, evidence-based decisions and a long-term plan, we can help your clients eliminate the worries around number three. It doesn’t happen overnight, but with patience your clients might never have to worry about money ever again. We only get one shot on Earth, so it’s essential they act now.

However, before making any major financial choices it’s vital that your clients seek professional advice to work out the best strategy to achieve their lifestyle goals and long-term plans.

Get in touch

If your clients potentially find themselves facing an effectively 60% Income Tax rate, it is important that they don’t panic and instead seek solutions. They should reach out for expert advice and contact us by email at info@grey-parrot.co.uk or call us at 02039 871782.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future results.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates and tax legislation may change in subsequent Finance Acts.

Production

Production